Today I’m sharing everything you need to know about Per Stirpes.

In fact, this confusing Latin word recently saved our client from sending over $500,000 to the wrong beneficiary.

(And she didn’t need an attorney to take action!)

If you want to ensure the right people inherit your hard-earned money, you’ll enjoy today’s article.

What Is Per Stirpes

Per stirpes is a legal term used in estate planning to ensure the assets of a deceased person are distributed fairly among their family members. It stems from Latin, meaning “by branch” or “by roots,” signifying that each family branch should receive an equal share of the estate.

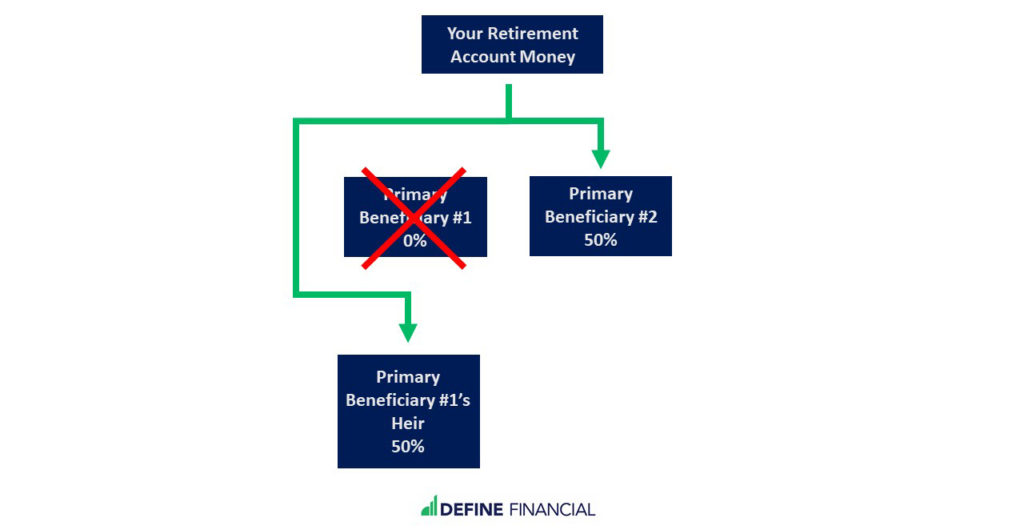

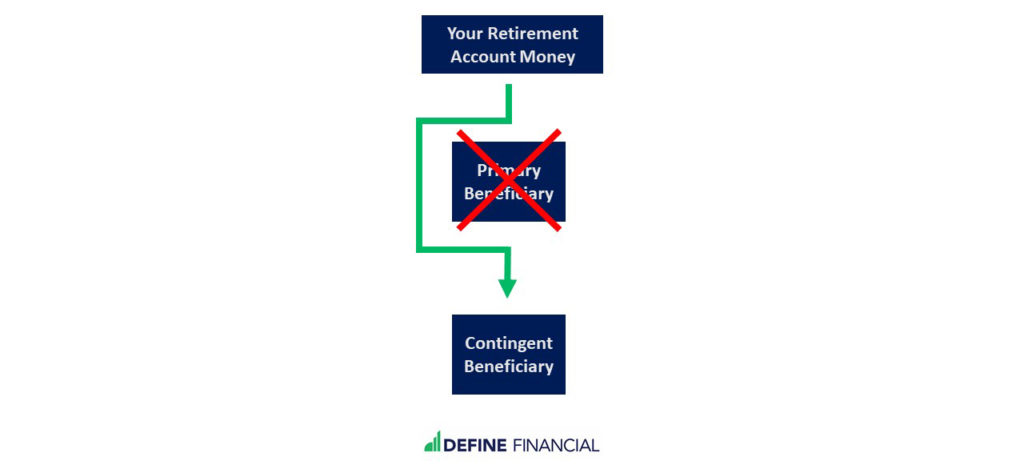

Per stirpes comes into play when one or more beneficiaries predecease the owner(s) of the estate. Put simply, if a beneficiary dies before you die, the deceased beneficiary’s children inherit your money.

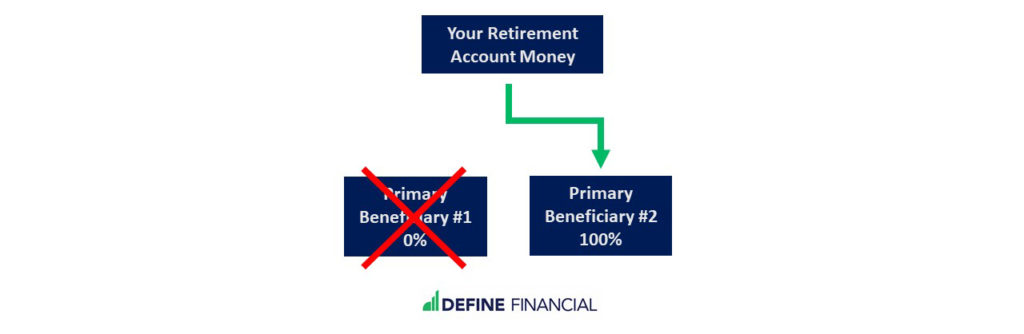

Without per stirpes, everything is passed to the remaining primary beneficiary.

It is essential to consider all aspects of your financial and personal situation when creating an estate plan. Including the per stirpes designation can help ensure your assets are distributed as you intended, maintaining fairness and clarity for your family and loved ones.

By considering the use of per stirpes when planning your estate and beneficiary designations, you can have peace of mind knowing that your family’s inheritance is well-planned and secure.

How Per Stirpes Works (Example)

To understand how per stirpes works, consider the following example.

Grandma Gloria has a $1 million retirement account. Her only remaining family members are her daughter and granddaughter.

Right now, her daughter is named as the primary beneficiary on her retirement account. In other words, when Grandma Gloria dies, her daughter will inherit the account.

However, if the daughter dies before the grandmother, the retirement account would not make it to the granddaughter.

That might make the granddaughter very sad.

More importantly, it might make the grandmother sad that her intentions weren’t carried out.

If, instead, the grandmother elects per stirpes – and her daughter dies before her – the money would go straight to the granddaughter.

Elect per stirpes on your retirement account beneficiary designations to ensure that your heirs’ heirs receive their share.

Electing per stirpes ensures that your assets are distributed according to your wishes and provides a clear roadmap for your loved ones. By employing this method, you can avoid potential disputes and complications, ensuring your estate’s distribution aligns with your intentions.

Setting Up Your Beneficiary Designations on Retirement Accounts

One important part of this planning is setting up your beneficiary designations.

What are beneficiary designations?

Beneficiary designations determine who gets your retirement account money when you pass away.

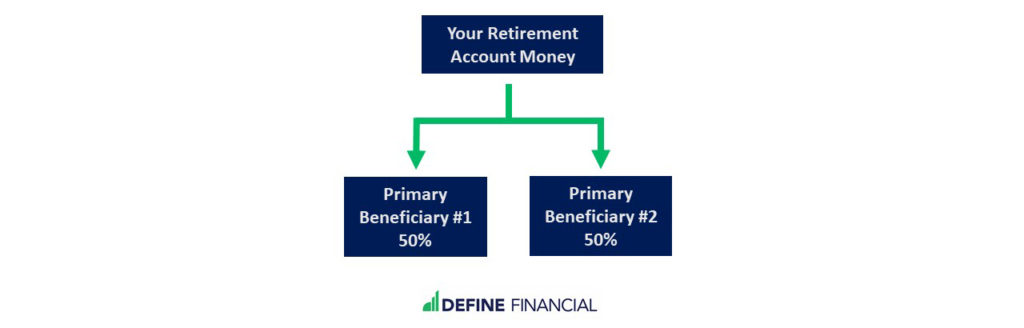

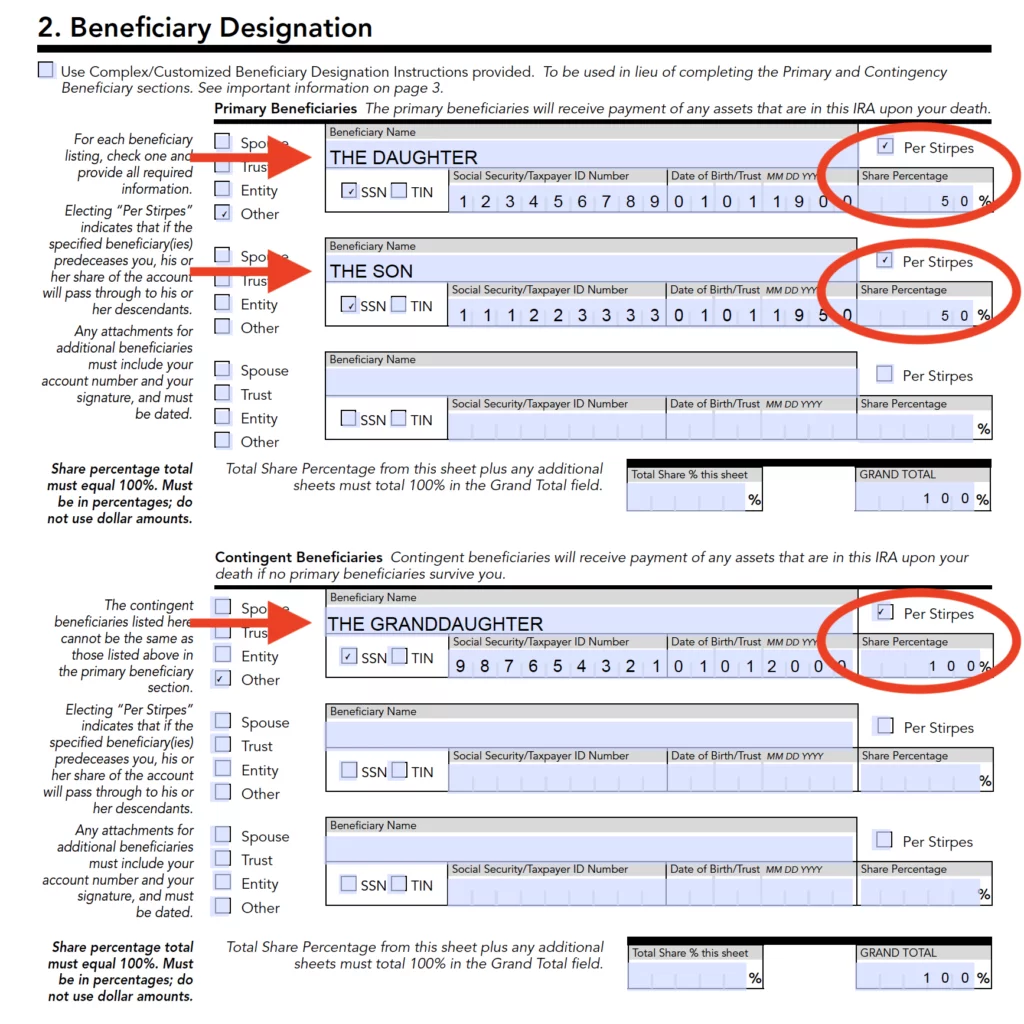

One example of how to set up your beneficiary designations – with two individuals receiving equal halves.

Your retirement accounts include your IRA accounts and your employer-sponsored retirement plans. This means:

- Traditional and Roth IRAs

- SIMPLE IRAs

- SEP IRAs

- Traditional and Roth 401(k)’s

- Traditional and Roth 403(b)’s

- Traditional and Roth 457’s

- 401(a) accounts…and more!

Primary vs Contingent Beneficiaries

Most married people opt for their spouse as their primary beneficiary.

If you do that, it means your spouse gets the money in your retirement accounts when you die.

This scenario is so commonplace that, if you are married and you don’t assign your spouse as the primary beneficiary, you will likely need some special paperwork to make that possible.

In other words, your spouse may need to sign a notarized document that says he/she is okay with not being the primary beneficiary on your retirement accounts.

Also, you will likely need to set up contingent beneficiaries for your retirement accounts.

If you’re married with kids, your contingent beneficiaries might be your children. If your primary beneficiary passes away before you do, your money will go to your contingent beneficiaries.

Contingent beneficiaries inherit your assets if the primary beneficiary passes before you do.

Per Stirpes vs Per Capita

A final consideration when setting up your beneficiary designations is whether to elect per stirpes or per capita.

What is Per Capita?

Per capita is typically the default option on most retirement accounts if per stirpes isn’t chosen.

Back to our example above, let’s say that the grandmother still has a daughter and granddaughter…but she also has a son.

The daughter and son are listed as 50/50 beneficiaries on the grandmother’s $1 million retirement account.

So, if grandma gets run over by a reindeer tomorrow, each would receive $500,000.

However, if the daughter gets run over first – and per capita was chosen by default – the $500,000 earmarked for the daughter will go to…the son!

The son would have $1 million dollars in his pocket and the granddaughter would be left with nothing.

Should I Use Per Stirpes for My Beneficiary Designations?

If you’re setting up the beneficiary designations on your retirement accounts, you will be faced with this very question.

“Should you use per stirpes?”

The right answer for you depends on several factors.

For example, do you want your money to pass to your beneficiary’s heirs? It’s possible this was your plan all along.

But, it’s also possible you don’t want your grandchildren to get access to your money.

One factor to consider is the age of the heirs who would receive the money via per stirpes.

For example, if you’re looking at passing assets to your children (and your grandchildren via per stirpes), consider the grandchildren’s ages.

Are the grandchildren minors? Would the grandchildren be able to manage your assets on their own?

These are not easy questions to answer.

This is why you may want to consult with a financial planner and estate attorney to help choose your beneficiary designations.

Step-by-Step: How to Elect Per Stirpes or Per Capita on Your Retirement Accounts

Step 1

Contact the bank or custodian where your retirement accounts are held (e.g. Fidelity, Vanguard, Morgan Stanley, etc.) and request a copy of your current beneficiary designations.

Review your current designations and do two things:

- Confirm what you currently have on file is correct and aligned with your intentions.

- Check to see if per stirpes has been selected. (Remember, per capita is typically chosen by default.)

If everything looks good, your job is done. If things are in need of updating, move to step 2.

Step 2

Every bank or custodian has a “beneficiary designation form.”

If you need to make a change to your beneficiaries – including per stirpes or per capita – you need to contact your bank or custodian and request this form.

(You can also contact your financial planner if you have one.)

With the beneficiary designation form in hand, you can make the appropriate changes to your beneficiary designations. It might look something like this:

Example of a beneficiary designation form where you can choose per stirpes.

In Conclusion

If you’re staring at the little per stirpes checkbox when you set up your next retirement account, pat yourself on the back.

More than half of U.S. adults do not have an estate plan and the numbers increase significantly for minority groups.

While planning for a future without you can be a difficult task, it is one of the most important pieces of a financial plan. And starting the process with setting up your beneficiary designations correctly can be a good place to start.

To summarize, if you’re assigning your children as your primary beneficiary and their children (your grandchildren) are well into their 30s – and capable of managing their own finances – then checking the per stirpes box may be an easy decision.

If your grandchildren are minors, then working with a financial planner and estate attorney to design a custom plan might be the prudent option.

The bottom line is that per stirpes should not be ignored.

It’s a critical piece of the retirement planning process that deserves to be reviewed every year, at minimum.